Berkshire Hathaway:

The implied volatility trends in the financial sector for March 2024 are influenced by various factors like economic indicators, Federal Reserve policies and market sentiment. The Federal Reserve’s stance on interest rates plays a crucial role in shaping these trends. Despite concerns about investor growth, the Fed seems inclined towards maintaining higher rates for an extended period rather than opting for rate cuts. This cautious approach could impact market expectations and potentially increase volatility if the unemployment rate continues to rise, which historically signals higher recession risks and consequently, elevated implied volatility levels.

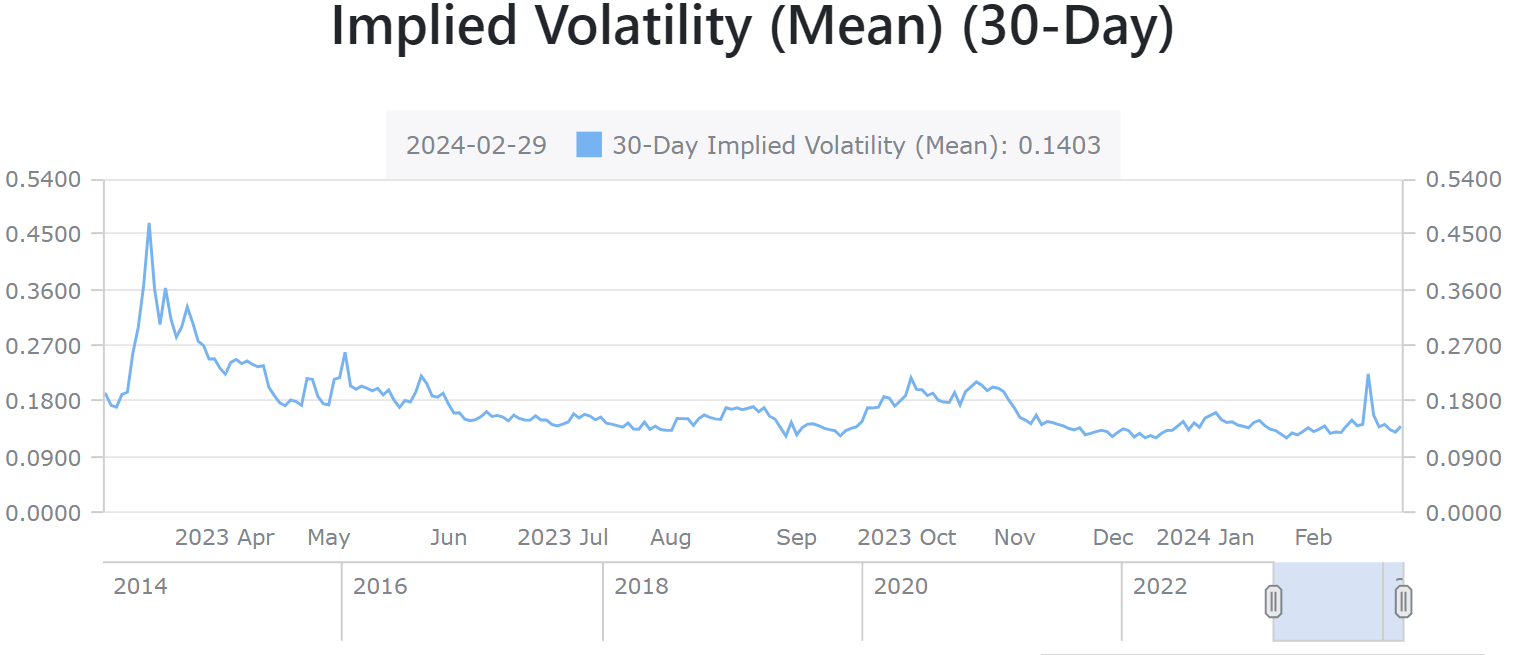

As of the end of February 2024, the Financial Select Sector SPDR ETF (XLF) exhibited an implied volatility (calls) of 0.1187, reflecting market expectations for future price fluctuations over the next 30 days. Comparing this metric with historical volatility data offers insights into potential movements in stock prices within the financial sector. Discrepancies between historical and implied volatility levels can indicate prevailing market sentiment; higher implied volatility typically signifies anticipated price shifts.

Looking ahead, J.P. Morgan Research anticipates only modest risk of a global recession in the near term but projects an end to the global expansion by mid-2025. Persistent inflation and the likelihood of higher-for-longer rates could disappoint current market expectations for an early start to developed market easing cycles. A challenging macro backdrop is expected for equity markets in 2024, with geopolitical risks and earnings growth potentially weighing on stock performance based only on Specific sectors like Technology. This outlook reflects a cautious stance on the performance of risky assets over the next 12 months due to monetary headwinds, geopolitical concerns, and, on average, expensive asset valuations.

In summary, the financial sector in 2024 appears to be at a complex crossroad where strategic stock-picking could offer value, especially in banks with quality deposits, capital markets-focused firms, and certain life insurers. The sector’s ability to adapt to technological advancements and a tighter regulatory environment will likely determine its resilience and potential for growth amidst these challenges.

Moreover, analyzing broader market dynamics and sector specific trends reveals that while implied volatility has risen across most sectors, overall levels have remained relatively subdued. This suggests that market participants are pricing in lower levels of expected price fluctuations for the upcoming month. In contrast, certain industries such as Energy showed increased implied volatility, while sectors like Technology had lower volatility expectations.