The outlook for the Q2 earnings season of 2024 is shaped by a mix of optimistic and cautious perspectives across different sectors and global markets.

U.S. Market and Economic Environment:

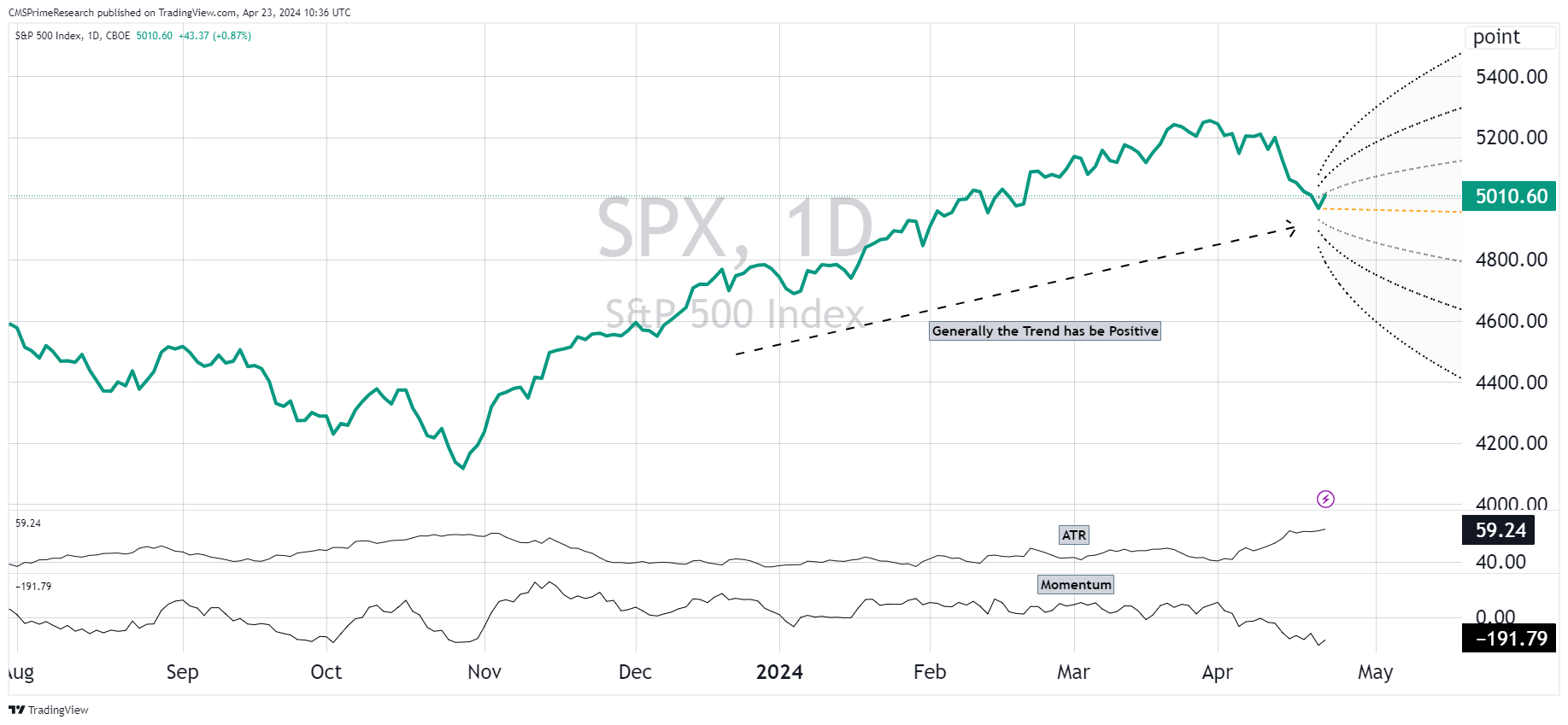

The U.S. stock market has shown resilience, with S&P 500 earnings growth expectations for 2024 revised upwards. The technology sector is anticipated to play a significant role, accounting for about half of this year’s S&P 500 earnings. This reflects an upbeat risk appetite, particularly around the integration and impact of artificial intelligence across various sectors.

However, the overall performance of risky assets and the macro outlook for the next year are viewed with caution due to ongoing monetary headwinds and geopolitical risks.

Global Economic Trends:

The global economic growth is expected to be slow, with challenges such as moderate growth and persistent inflation affecting market dynamics.

Japan presents a brighter scenario with solid corporate earnings and supportive monetary policies, making it a favorable market for investors.

Labor Market and GDP Growth:

U.S. GDP growth is expected to normalize by the fourth quarter, but a slowdown is anticipated for 2024. The labor market is expected to experience a modest uptick in unemployment, though severe impacts like a recession are not anticipated.

Inflation and Interest Rates:

Inflation is expected to ease, and with it, interest rates might see adjustments. The U.S. has experienced what some analysts call “immaculate disinflation,” where inflation rates have fallen without significant harm to the economic cycle, largely due to improvements in supply chains and labor market recoveries. The inflation rate in the US stands at 3.48%, a slight increase from 3.15% in February. The annual increase is lower compared to 4.98% a year ago, marking a significant easing of inflation over the year.

Overall, while there are positive indicators like technological advancements and supportive policies in certain regions, the broader picture remains mixed with potential risks from inflation, interest rates, and geopolitical tensions. This sets a stage for cautious optimism with a focus on strategic, nimble investment approaches as the economic and market conditions evolve.

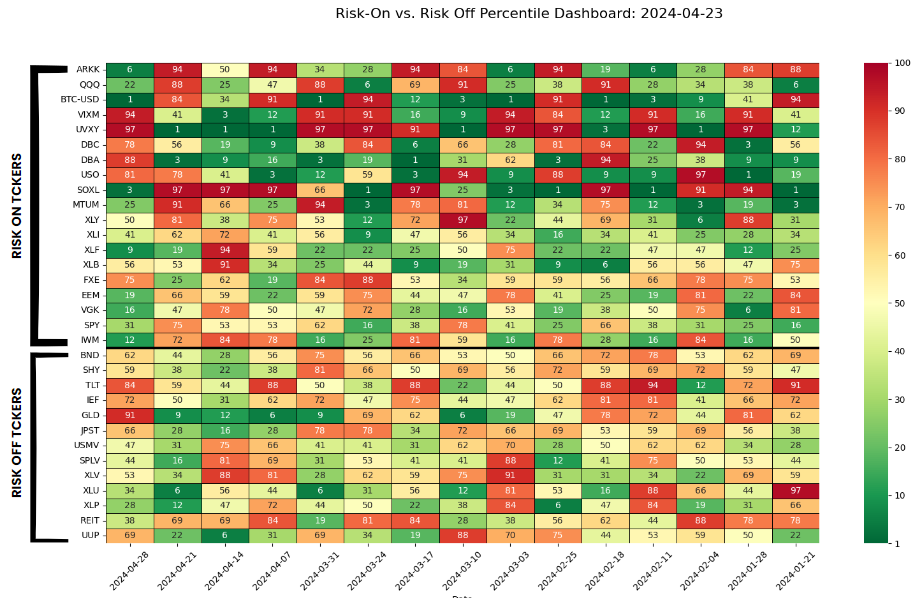

Equity-Linked ETFs and Assets

- ARKK & QQQ: Initially, these ETFs showed a strong risk-off sentiment (reds and oranges), indicating skepticism towards growth stocks. Over the months, there seems to be an intermittent shift towards risk-on (greens), possibly due to earnings optimism or a shift in tech sector outlook.

- MTUM: This momentum-based ETF has fluctuated but shows a trend towards risk-on, indicating a return to favoring high-momentum stocks.

Volatility Indexes

- VIXM & UVXY: Both started with high risk-off sentiment but moved towards a more neutral stance. The initial fear indicated by deep reds could have been due to geopolitical tensions or market volatility, which appears to have subsided, leading to less reliance on volatility hedges.

Commodities

- USO & DBC: Strong risk-on sentiment, especially in USO, may reflect expectations for economic growth or inflationary pressures, making commodities an attractive bet. Over three months, this sentiment remained largely consistent.

Fixed Income and Safe-Haven Assets

- TLT & IEF: These assets, which often signal risk-off moves, showed a consistent preference for risk-off, potentially due to interest rate hike expectations or economic uncertainty.

- GLD: The preference for gold, a classic safe-haven asset, fluctuated but ended on a stronger risk-off note, possibly due to increased market uncertainties or inflation fears.

Over the past three months, the market sentiment oscillated but appears to have reached a more balanced state with both risk-on and risk-off signals across different asset classes.

Current Market Position: Risk-On or Risk-Off?

- The overall market sentiment currently leans towards risk-on, particularly in equities and commodities, despite some persisting caution as indicated by fixed income and safe-haven assets.

- The presence of both risk-on and risk-off sentiments suggests a market at a crossroads, reflecting a mix of optimism about economic recovery and concerns over inflation, interest rates, and geopolitical issues

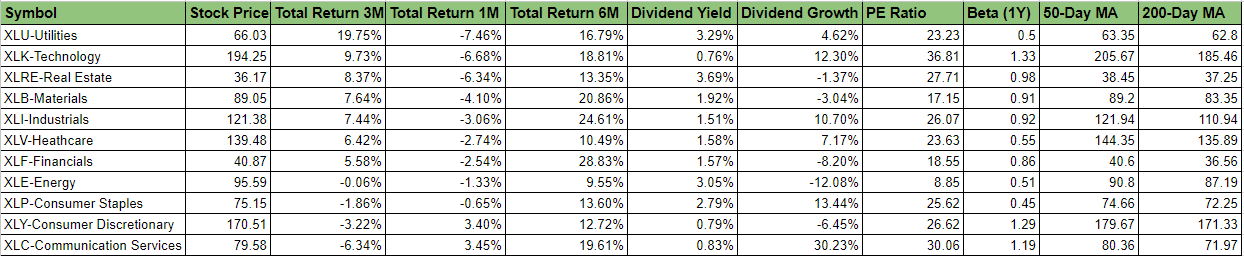

Valuations and Justifications Across Sectors:

General Trends

- Returns: The past 3-month, 1-month, and 6-month returns show varying performance across sectors with technology and communication services leading in 3-month returns and Financials in 6-month returns.

- Dividends: Dividend yields vary, with energy providing the highest yield. Dividend growth is robust in sectors like technology and communication services but negative for financials and energy.

- Volatility: Betas show that utilities, healthcare, and consumer staples are less volatile sectors, while technology, consumer discretionary, and communication services exhibit more volatility.

- Valuation: PE ratios indicate that energy is the most undervalued or least growth-expected sector, while communication services are the most highly valued in terms of growth expectations.

Geopolitical Factors and Election Cycles: The political landscape, particularly in the U.S., with an upcoming election, is influencing sector-specific behaviors, notably within green energy sectors, which are highly sensitive to policy changes. Such sectors show heightened activity in discussions around potential regulatory changes that could arise from election results.

Sectoral Opportunities: Specific sectors such as healthcare and technology appear poised for growth, driven by innovation and the ongoing digital transformation. However, the performance is closely tied to broader economic indicators and investor sentiment, which are currently mixed due to the ongoing macroeconomic adjustments.

Emerging Market Divergence: Emerging markets are showing a divergent growth pattern, with some regions potentially offering lucrative opportunities due to less stringent monetary policies and different stages of economic recovery post-pandemic.