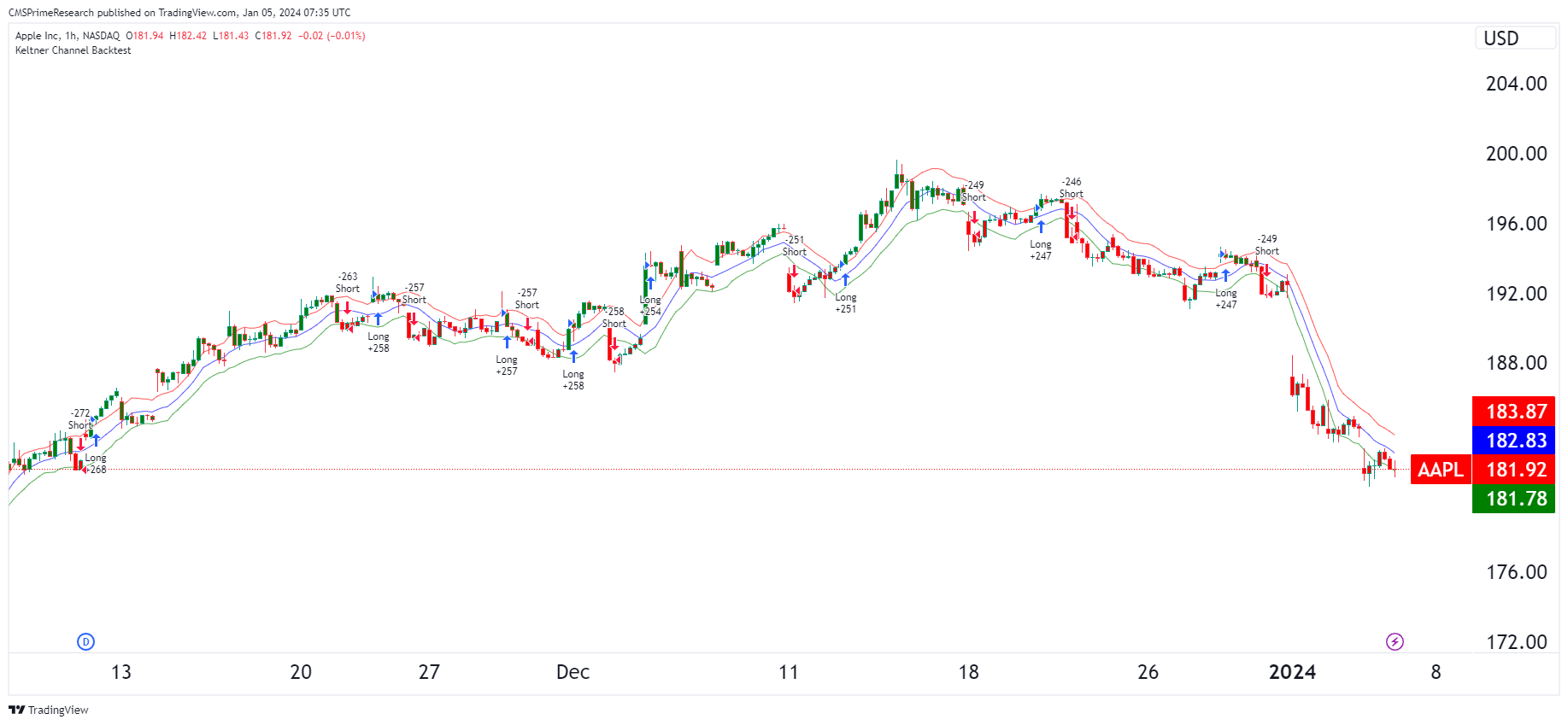

In this particular backtest, you can see instances where “Long” and “Short” positions are suggested:

- A Long signal is typically indicated when the price moves above the upper Keltner Channel, suggesting a strong upward momentum and a bullish sentiment, prompting traders to consider buying or holding a position.

- A Short signal is indicated when the price drops below the lower Keltner Channel, signaling a strong downward momentum and a bearish sentiment, where traders might consider selling or shorting a position.

Dynamics of Comparisons

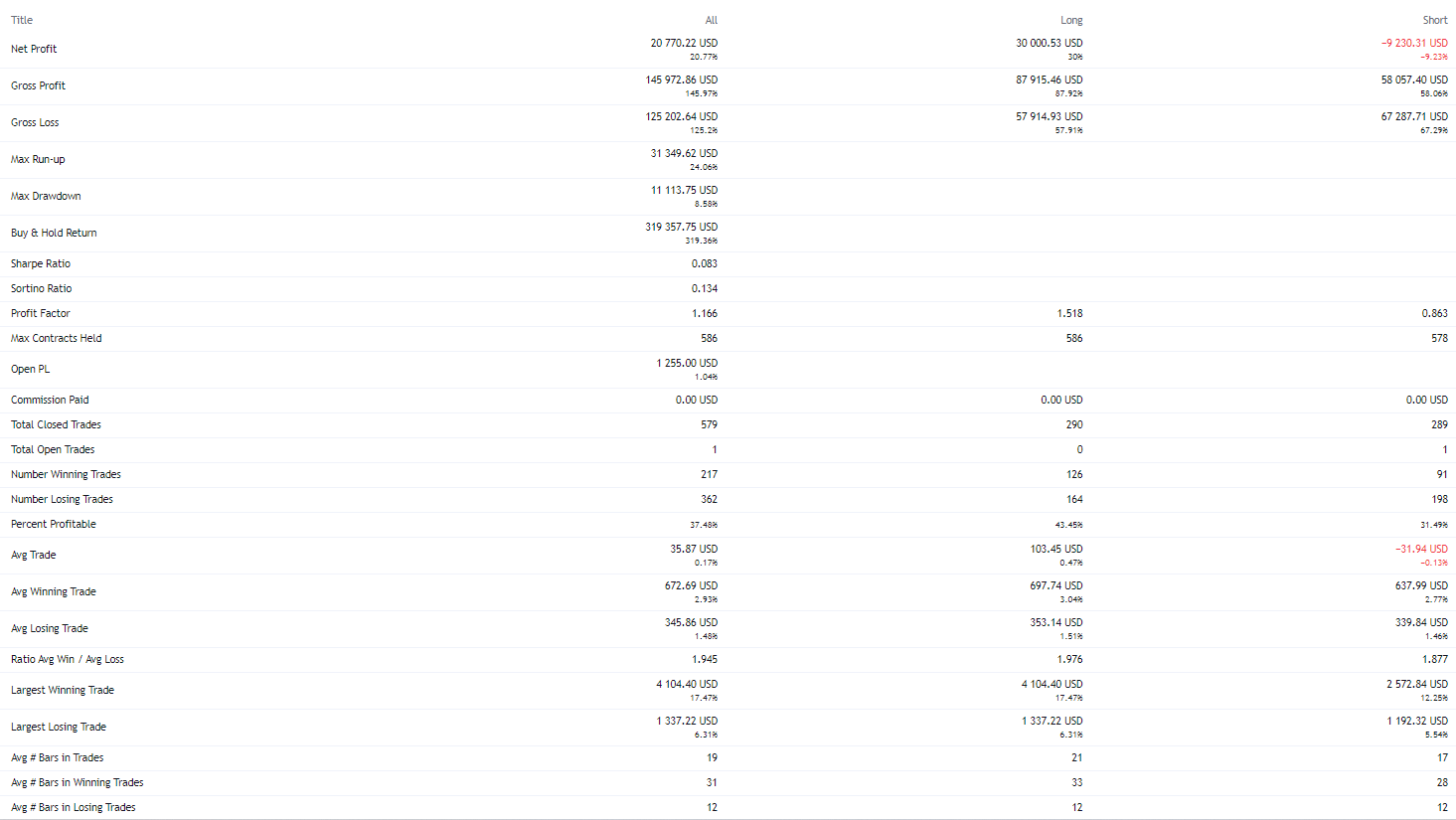

Profit Factor: The Long trades have a higher profit factor (1.518) compared to Short trades (0.863), suggesting that Long trades are more profitable overall.

Profitability: While the overall percent profitable is not high (37.48%), the Long trades seem to be doing better in terms of net profit, indicating a bullish bias in the strategy’s effectiveness.

Average Trade Results: The average winning trades are relatively similar for Long and Short, but the average losing trade is slightly higher for Long trades. This could suggest that while the strategy is profitable, the risks associated with Long positions might be higher.

Ratios: The higher ratio of average win to average loss in Long trades (1.978) compared to Short trades (1.877) indicates a better performance of the Long strategy.

Largest Trades: The largest winning trades are the same for All and Long, suggesting that the most significant gains come from Long positions. However, the largest losing trades are relatively close, indicating that losses can be significant in both directions.

Long-Term Viability and Bias Recognition

Given the positive net profit for Long trades and a negative one for Short trades, the strategy seems to exhibit a bullish bias. The Long trades not only yielded more gross profit but also managed to maintain a higher profit factor despite the losses. This suggests that in the long run, the strategy could be effective if the market conditions that favor Long positions persist. However, the relatively low Sharpe and Sortino ratios for the overall strategy indicate that the returns are not significantly high when adjusted for risk, which may question the strategy’s attractiveness for risk-averse investors.

Comparative Complexity

If one aspect, like the profit factor, is low (as it is for Short trades), it could mean that the strategy isn’t as effective or robust against market downturns. However, if the profit factor is high for Long trades, this demonstrates the strategy’s potential under favorable market conditions. The complexity arises in managing the risks and recognizing when to shift bias from bullish to bearish based on market dynamics.

The strategy appears to have a stronger performance in Long trades compared to Short trades, suggesting a bullish bias. While the strategy has demonstrated profitability, its long-term success will depend on consistent risk management and the ability to adapt to changing market conditions. The Sharpe and Sortino ratios point to a need for a careful assessment of risk versus return. This analysis indicates that the strategy has been more effective in Long positions but also carries inherent risks that must be carefully weighed.