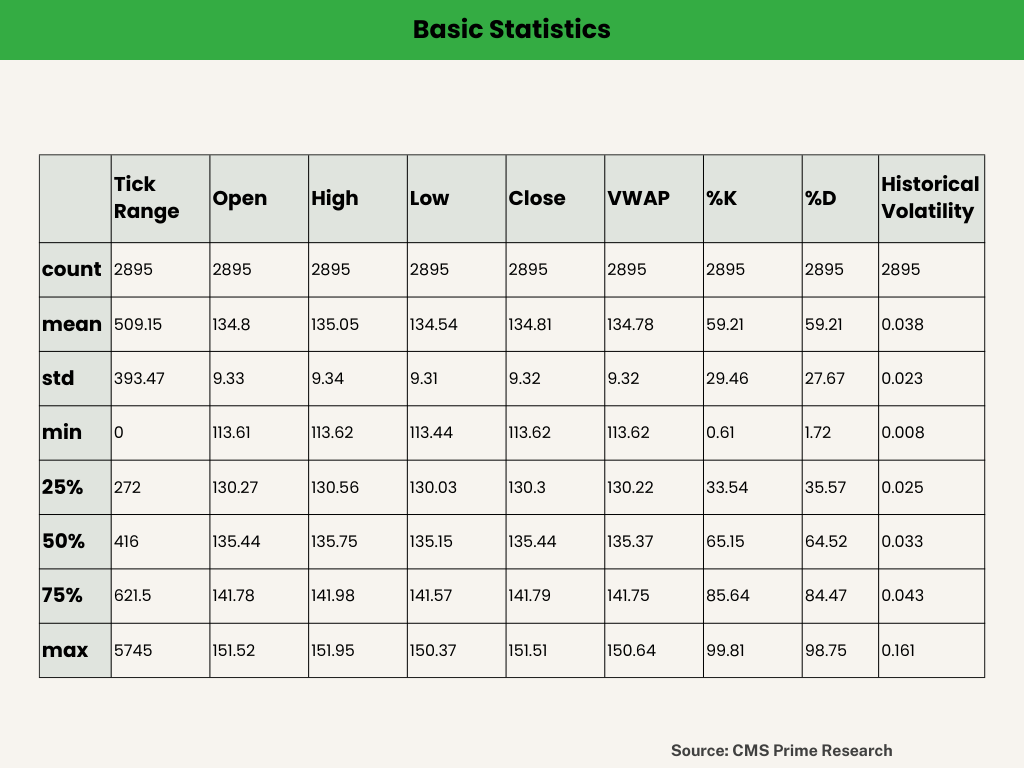

Understanding Historical Volatility and Volume Weighted Average Price (VWAP) is crucial for traders and investors as these metrics provide valuable insights into market trends and risk levels.

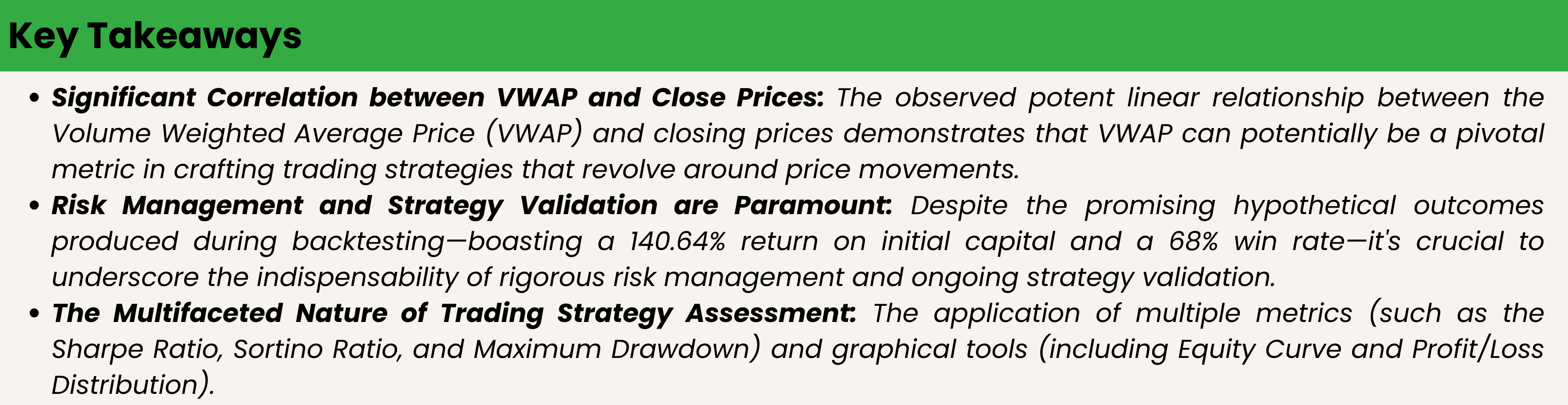

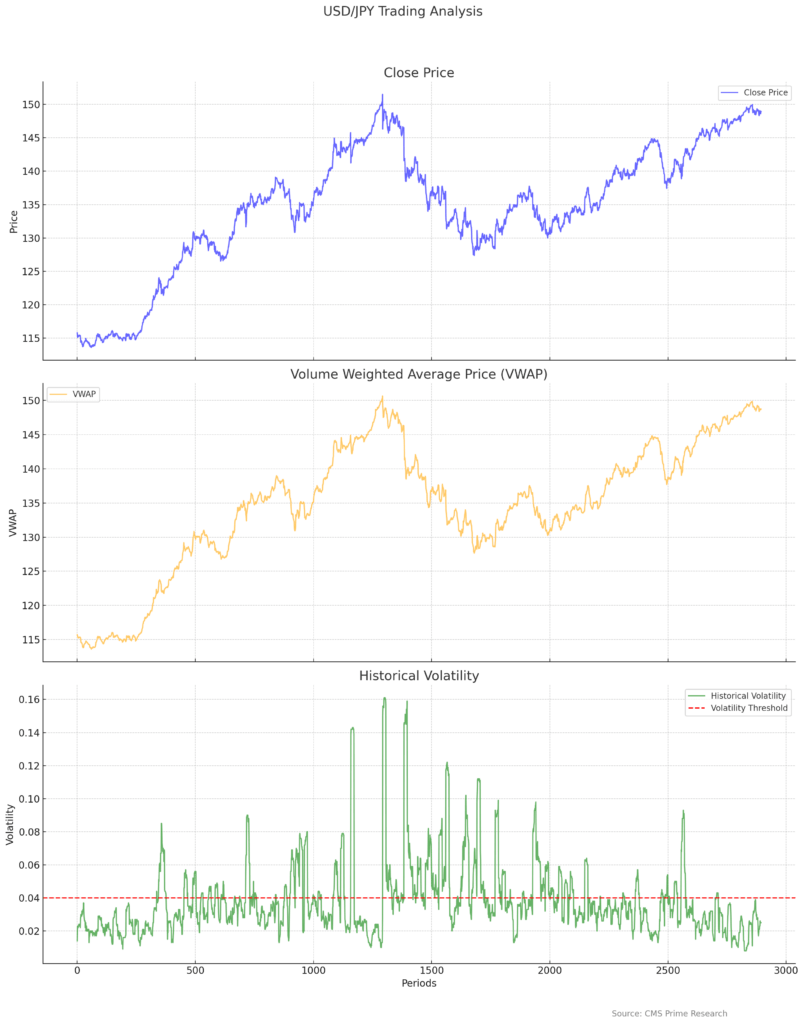

Historical Volatility (HV) is a statistical measure of the dispersion of returns for a given security or market index over a specific period of time. It is calculated by determining the average deviation from the average price of a financial instrument in the given time period. The higher the historical volatility value, the riskier the security. However, risk can work both ways—bullish and bearish. Historical volatility does not specifically measure the likelihood of loss, but it does measure how far a security’s price moves away from its mean value. This measure is frequently compared with implied volatility to determine if options prices are over- or undervalued. Historical volatility is also used in all types of risk valuations. Stocks with a high historical volatility usually require a higher risk tolerance. High volatility markets also require wider stop-loss levels and possibly higher margin requirements.

On the other hand, Volume Weighted Average Price (VWAP) is a tool that traders use to track the average price of a security over a certain period of time. VWAP gives traders insight into how a stock trades for that day and determines, for some, a good price at which to buy or sell. It can also help traders and analysts gain insight into where the momentum is at a specific time frame. For example, if a stock reverses and has a clean breakout above the VWAP, the trader should look to cover the short because they may be on the wrong side of the trade; the momentum has shifted to the buy side because the sellers have let up.

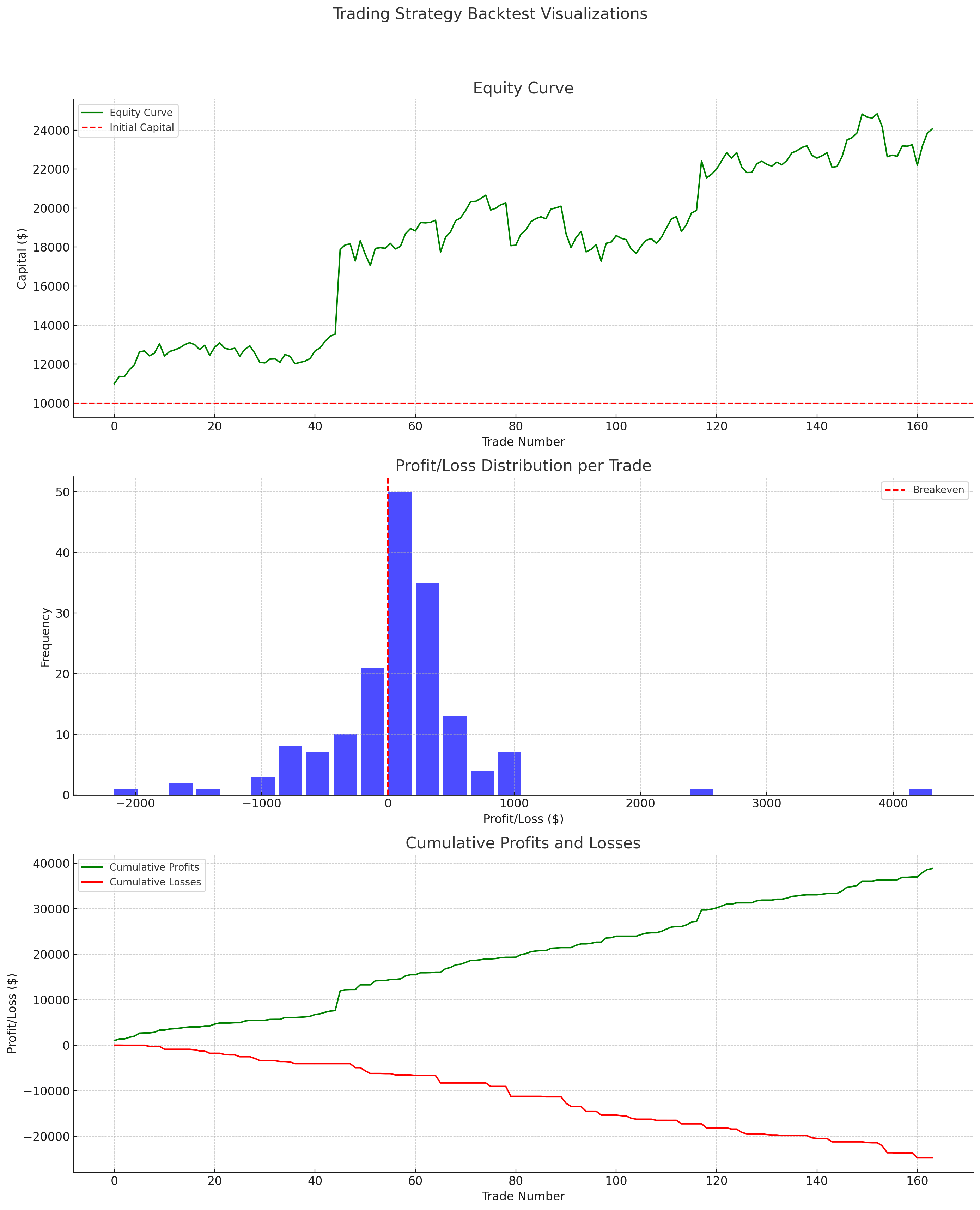

In conclusion, understanding Historical Volatility and VWAP is essential for traders and investors as it helps them make informed decisions about their investments. These metrics provide insights into market trends, risk levels, and potential investment opportunities.