Volatility is a statistical measure of the dispersion of returns for a given security or market index. In finance, volatility is often measured using the standard deviation of logarithmic returns. To understand and visualize the volatility of EUR/USD and GBP/USD:

Calculate Log Returns:

where rt is the return at time t, Pt is the price at time t, and Pt−1 is the price at time t−1.

Compute Rolling Volatility: Calculate the rolling standard deviation of the log returns using a specified window (e.g., 20, 50, or 200 days) to get a moving measure of volatility.

Visualize Volatility: Plot the computed rolling volatility to visualize how it has changed over time for both currency pairs.

Firstly lets calculate the log returns and visualizing them alongside the original price data. Then, we’ll compute and visualize the rolling volatility.

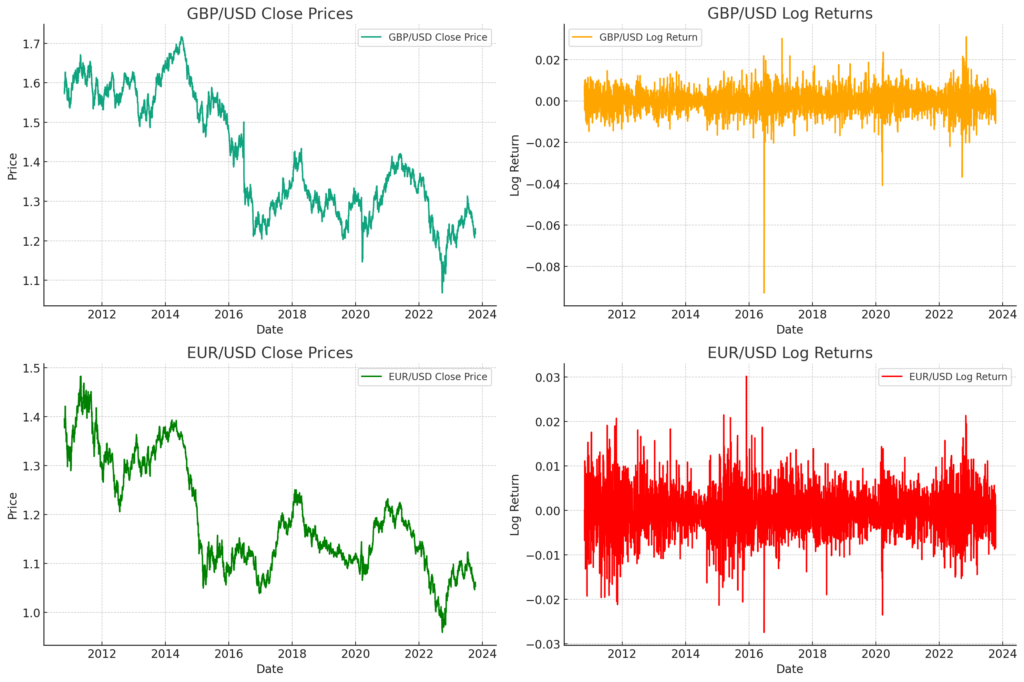

The plots above illustrate the following:

- Top Left: The GBP/USD close prices over time.

- Top Right: The logarithmic returns of GBP/USD.

- Bottom Left: The EUR/USD close prices over time.

- Bottom Right: The logarithmic returns of EUR/USD.

Logarithmic returns provide us with a continuous compounding return between two price points and tend to be normally distributed, which is a useful property for statistical analysis