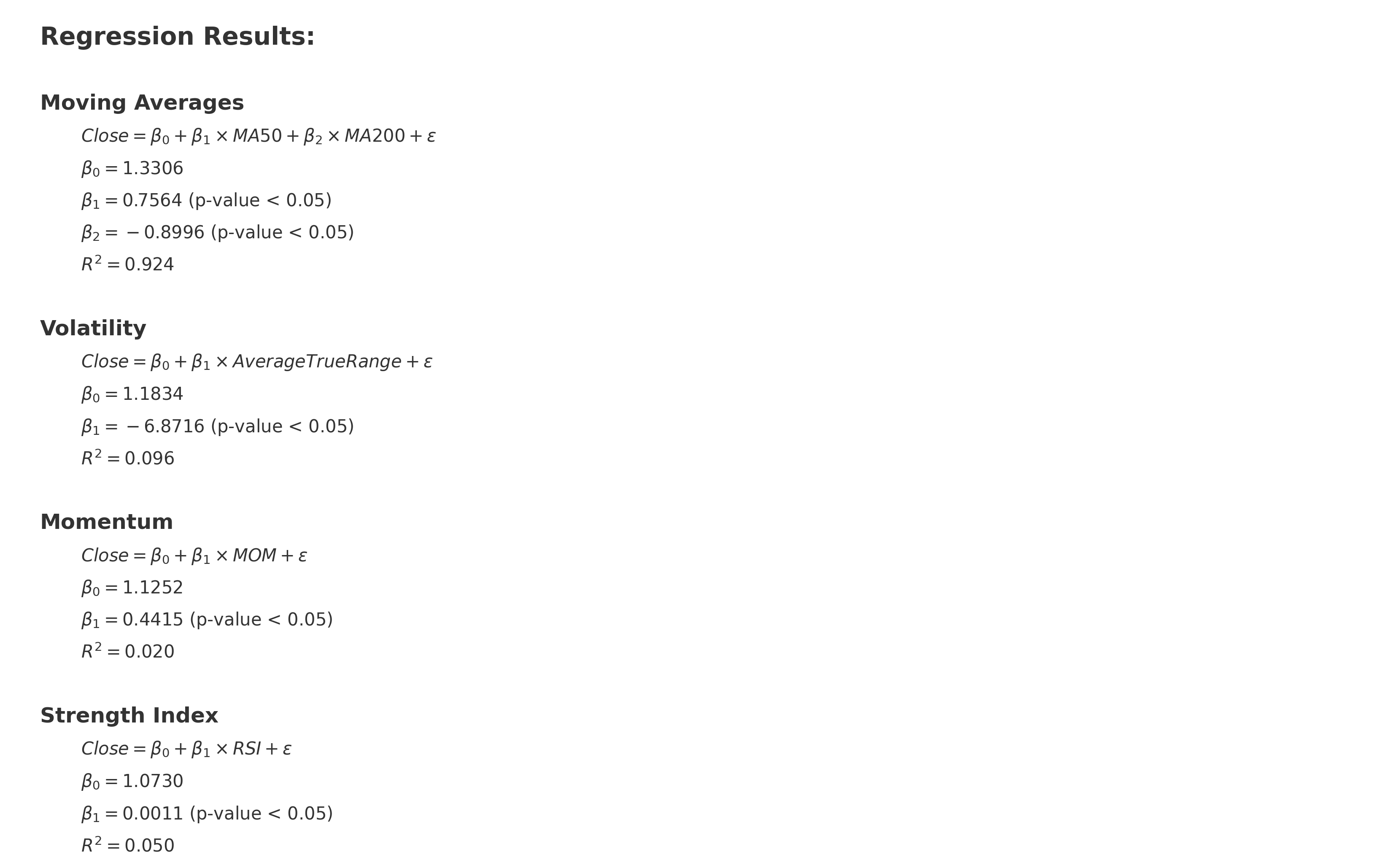

The regression results for the Moving Averages Hypothesis are:

Where:

- is the error term.

- , indicating that approximately 87.6% of the variation in the closing price is explained by the model.

Regarding the p-values (P>|t|) for the coefficients:

- The p-value for MA50 is 0.000, which is less than 0.05, indicating that MA50 is statistically significant in predicting the closing price.

- The p-value for MA200 is also 0.000, which is less than 0.05, suggesting that MA200 is statistically significant in predicting the closing price.

Thus, we reject the null hypothesis H0 for both MA50 and MA200, accepting the alternative hypothesis H1 that states there is a significant relationship between the moving averages (MA50 and MA200) and the closing price.

The regression results for the Volatility Hypothesis are:

Where:

- is the error term.

- , indicating that approximately 9.6% of the variation in the closing price is explained by the model.

Regarding the p-value (P>|t|) for the coefficient:

- The p-value for Average True Range is 0.000, which is less than 0.05, indicating that the Average True Range is statistically significant in predicting the closing price.

Thus, we reject the null hypothesis H0 for the Average True Range, accepting the alternative hypothesis H1 that states there is a significant relationship between the Average True Range and the closing price.

The regression results for the Momentum Hypothesis are:

Where:

- is the error term.

- , indicating that only about 2% of the variation in the closing price is explained by the model.

Regarding the p-value (P>|t|) for the coefficient:

- The p-value for MOM is 0.000, which is less than 0.05, indicating that the Momentum (MOM) is statistically significant in predicting the closing price.

Thus, we reject the null hypothesis H0 for MOM, accepting the alternative hypothesis H1 that states there is a significant relationship between the Momentum (MOM) and the closing price.

The regression results for the Strength Index Hypothesis are:

Where:

- is the error term.

- , indicating that only about 5% of the variation in the closing price is explained by the model.

Regarding the p-value (P>|t|) for the coefficient:

- The p-value for RSI is 0.000, which is less than 0.05, indicating that the Relative Strength Index (RSI) is statistically significant in predicting the closing price.

Thus, we reject the null hypothesis H0 for RSI, accepting the alternative hypothesis H1 that states there is a significant relationship between the Relative Strength Index (RSI) and the closing price.

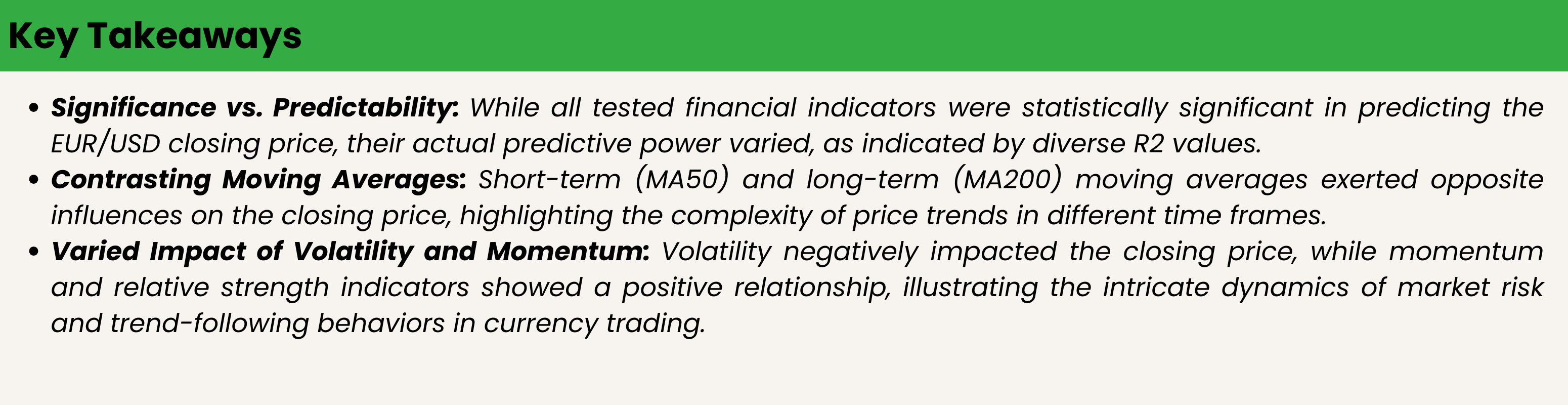

In Summary:

- All the independent variables (“MA50”, “MA200”, “Average True Range”, “MOM”, and “RSI”) were found to be statistically significant in predicting the closing price based on the p-values obtained from the regression analyses.

- However, the R2 values for the models (especially for “Average True Range”, “MOM”, and “RSI”) are quite low, suggesting that although the variables are statistically significant, they may not be strong predictors for the closing price.