First and foremost, the Eurozone’s Consumer Price Index (CPI) for September holds immense significance for the EUR/USD pair. Any substantial deviation from the consensus CPI figure of 124.9 could send ripples through the market. A higher-than-expected CPI may suggest a looming inflationary threat, potentially bolstering the Euro (EUR) by raising expectations of European Central Bank (ECB) tightening. Conversely, a figure below consensus might raise concerns about subdued inflation, possibly leading to a depreciation of the EUR against the US Dollar (USD).

Another pivotal metric to watch is the year-on-year (YoY) inflation rate in the Eurozone for September. Should this rate surpass the consensus of 4.50%, it could propel the EUR upwards against the USD, signaling a potential tightening of ECB monetary policy. Conversely, a figure below consensus may weaken the EUR against the USD, as it might indicate reduced pressure on the ECB to make adjustments to policy rates.

Turning to the United States, the US Core Personal Consumption Expenditures (PCE) Price Index for August is of utmost importance for the EUR/USD pair. Any substantial deviation from the consensus figure of 0.20% has the potential to sway market sentiment. A higher-than-expected Core PCE may strengthen the USD, as it reflects inflationary pressures and the possibility of action by the Federal Reserve (Fed). Conversely, a figure below consensus may weaken the USD, signaling muted inflation and dovish expectations regarding Fed policy.

The US Goods Trade Balance data for August is yet another factor that can exert influence on the EUR/USD pair. A trade balance better than the consensus deficit of -$95 billion may lend support to the USD, indicating a stronger economic position. However, a larger deficit might weaken the USD, sparking concerns about the US trade position and potentially leading to an appreciation of the EUR/USD exchange rate.

Finally, the Michigan Consumer Sentiment Index for September serves as a crucial gauge of sentiment in the United States. Any significant deviation from the consensus sentiment of 67.7 can impact market perceptions. Positive sentiment data may bolster the USD, suggesting robust consumer confidence, while lower sentiment figures could lead to a depreciation of the USD against the EUR.

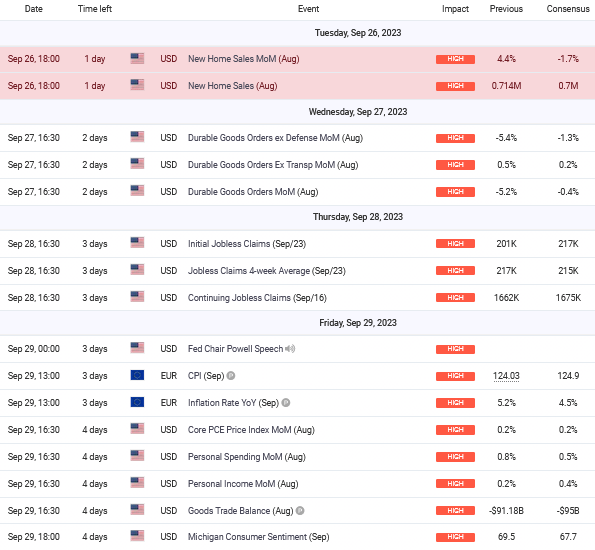

Technical Summary:

EUR/USD is bearish on the weekly chart, below 50 and 200-day moving averages.

Scenario 1: If it rises, it may test 1.06700 to 1.06964, then 1.07273 and 1.07649, possibly reaching 1.08004 and 1.08231.

Scenario 2: A reversal could test 1.06300, then 1.06359 and 1.06099. Further down, 1.05867 to 1.05678, with 1.05449 as strong support.

RSI is in a bearish oversold range with decreasing weekly momentum.

First and foremost, the Eurozone’s Consumer Price Index (CPI) for September holds considerable sway over the GBP/USD pair. Any notable deviation from the consensus CPI figure of 124.9 could yield substantial consequences. Should the CPI exceed expectations, it may signal mounting inflation, potentially strengthening the British Pound (GBP) as market participants anticipate a more hawkish stance from the Bank of England (BoE). Conversely, a figure below consensus might raise concerns about sluggish inflation, potentially leading to a depreciation of the GBP against the US Dollar (USD).

Equally critical is the year-on-year (YoY) inflation rate in the Eurozone for September. If this rate surpasses the consensus of 4.50%, it could drive appreciation of the GBP against the USD, suggesting the possibility of BoE tightening. Conversely, a figure below consensus may weaken the GBP against the USD, signifying reduced pressure on the BoE to adjust interest rates.

Shifting our focus to the United States, the US Core Personal Consumption Expenditures (PCE) Price Index for August plays a pivotal role in influencing the GBP/USD pair. Any significant deviation from the consensus figure of 0.20% could sway market sentiment. An above-expectation Core PCE figure may bolster the USD, reflecting inflationary pressures and potential actions by the Federal Reserve (Fed). Conversely, a figure below consensus may weaken the USD, indicating subdued inflation and dovish expectations regarding Fed policy.

Technical Summary:

GBP/USD shows weekly bearish momentum below 50 and 200-day moving averages.

Scenario 1: Retest of 1.2320 could lead to 1.2467, passing 1.2333, 1.2364, 1.2391, and 1.2429.

Scenario 2: Downside movement targets 1.2215, potentially 1.2186 and 1.2148, then a range of 1.2120 to 1.20005, with 1.2120 as strong support.

RSI near oversold, momentum currently down, but watch for possible bullish pullback.

Firstly, the US Core Personal Consumption Expenditures (PCE) Price Index for August holds a pivotal role in influencing the USD/JPY pair. Any significant deviation from the consensus figure of 0.20% could have a notable impact on market sentiment. Should the Core PCE exceed expectations, it may bolster the USD, reflecting inflationary pressures and the potential for Federal Reserve (Fed) actions. Conversely, a figure below consensus may weaken the USD, signaling subdued inflation and dovish expectations regarding Fed policy.

The US Goods Trade Balance data for August is another influential factor for the USD/JPY pair. If the trade balance performs better than the consensus deficit of -$95 billion, it could lend support to the USD, indicating a stronger economic position. However, a larger deficit may weaken the USD, raising concerns about the US trade position and potentially leading to depreciation of the USD/JPY exchange rate.

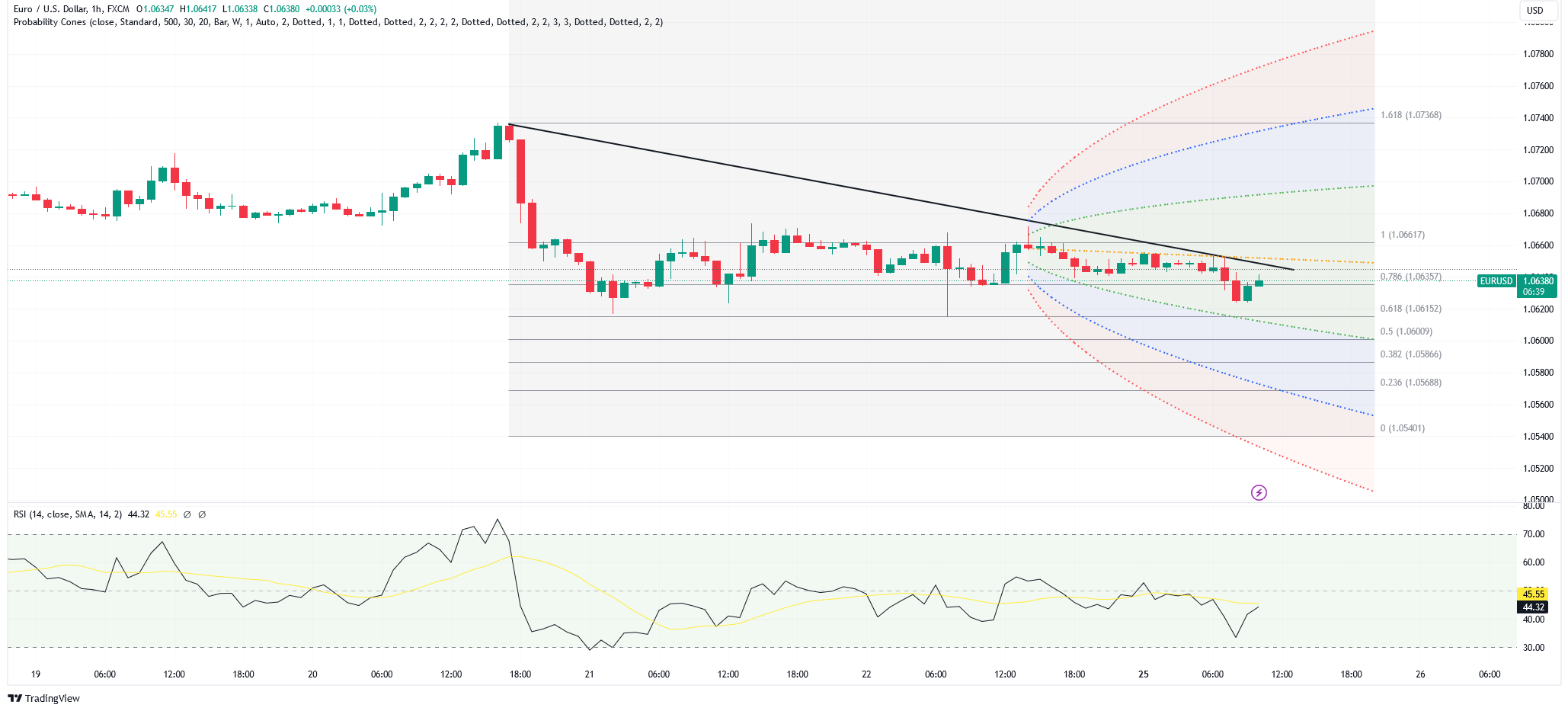

Technical Summary:

USD/JPY has bearish range momentum between 50 and 200-day moving averages.

Scenario 1: Downside targets 148.112, 147.822 (61.8% Fibonacci), then 147.548 to 147.231, with 146.934 and 146.670 as key support levels.

Scenario 2: Upside potential with retest of 148.404, aiming for 148.711 to 148.913, and possibly 149.430.

RSI is overbought but may enter a range, maintaining a long-term bullish momentum.

Firstly, the US Core Personal Consumption Expenditures (PCE) Price Index for August carries particular significance for Gold. Any notable deviation from the consensus figure of 0.20% could have a significant impact on market sentiment. If the Core PCE exceeds expectations, it may strengthen the US Dollar (USD), potentially putting downward pressure on the price of Gold as investors turn to USD-denominated assets. Conversely, a figure below consensus may weaken the USD, potentially providing support for the price of Gold.

The US Goods Trade Balance data for August also has implications for the price of Gold. Should the trade balance outperform the consensus deficit of -$95 billion, it could lend support to the USD and potentially lead to downward pressure on the price of Gold. However, a larger deficit may weaken the USD, potentially supporting the price of Gold as a safe-haven asset.

Finally, the Michigan Consumer Sentiment Index for September serves as another important factor. Any significant deviation from the consensus sentiment of 67.7 can sway market perception. Positive sentiment data may support the USD and potentially weigh on the price of Gold, as investors seek riskier assets. Conversely, lower sentiment figures could weaken the USD, potentially providing support for the price of Gold as a safe-haven asset.

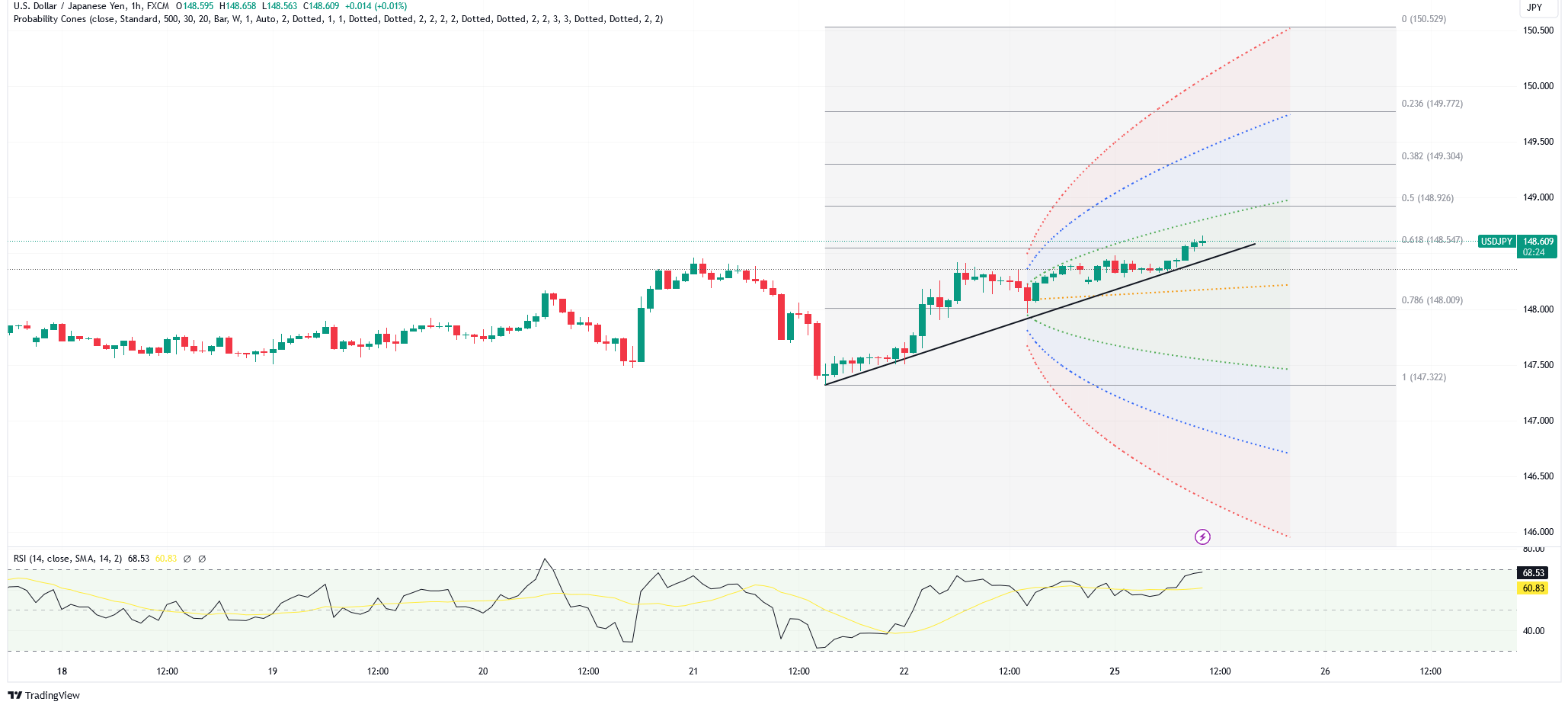

Technical Summary:

Weekly gold chart: Bearish downtrend but long-term bias is bullish. Near 200-day and 50-day moving averages, showing neutral sentiment.

Scenario 1: Potential rise to 1928, then 1933.50. Further bullish momentum may test 1940 and key level at 1950.

Scenario 2: Possible decline to 1920, then 1913 as major support. More bearishness targets 1908 and 1901.

RSI in undecided zone, overall momentum bearish, but a price range may include a possible upward pullback.