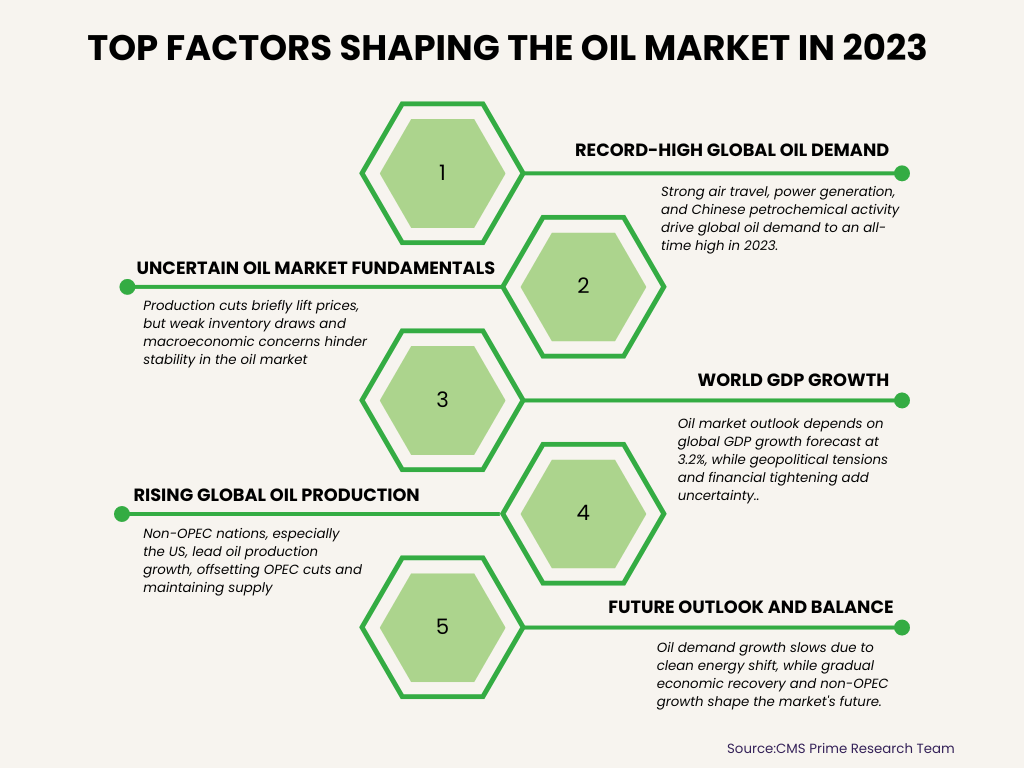

The Top 4 factors affecting the Oil Market trends are:

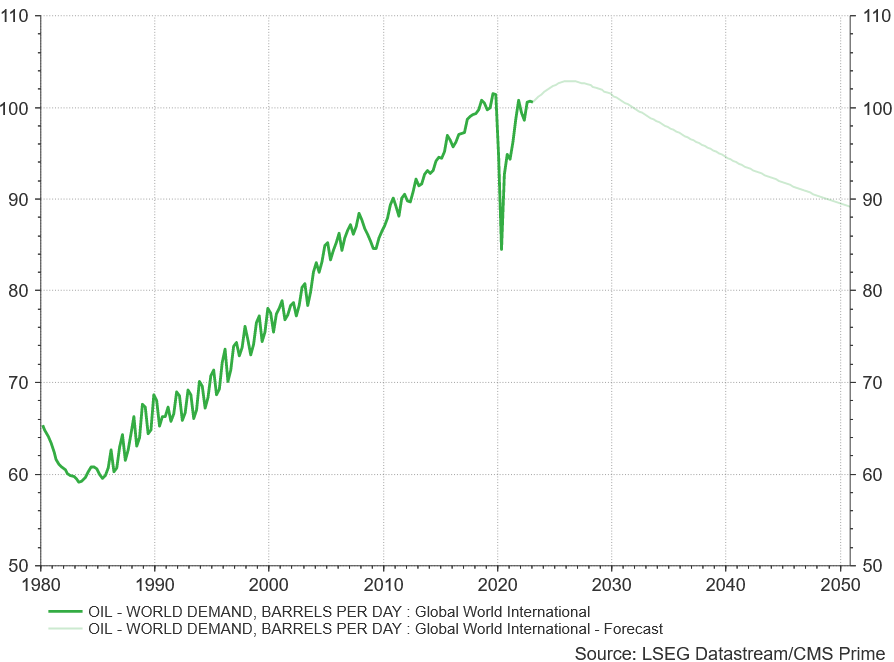

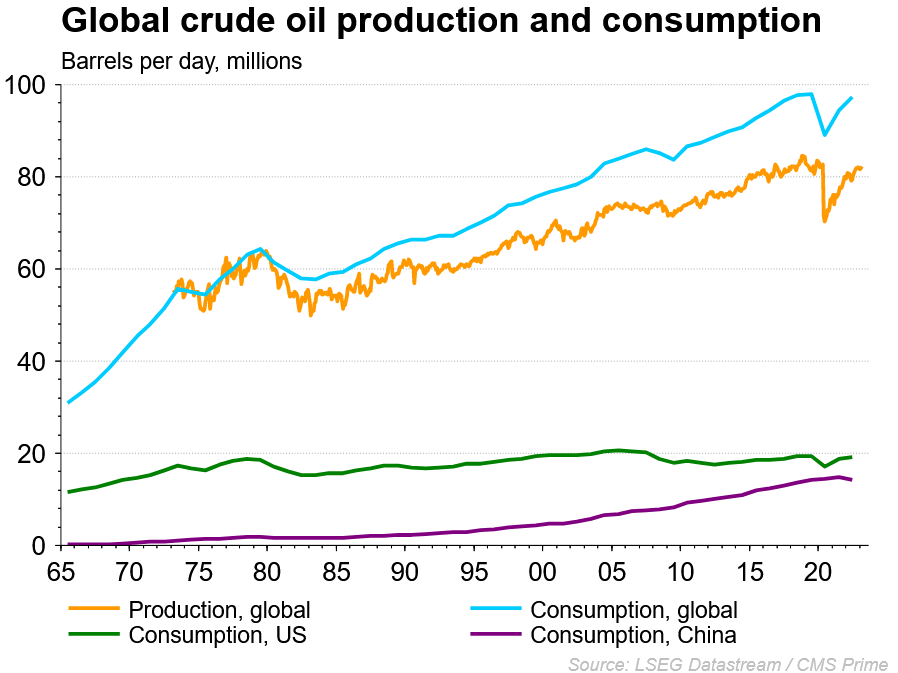

- Record-high global oil demand: World oil demand is reaching record highs, driven by strong summer air travel, increased oil use in power generation, and surging Chinese petrochemical activity. Global oil demand is set to expand by 2.2 million barrels per day (mb/d) to 102.2 mb/d in 2023, with China accounting for more than 70% of growth.

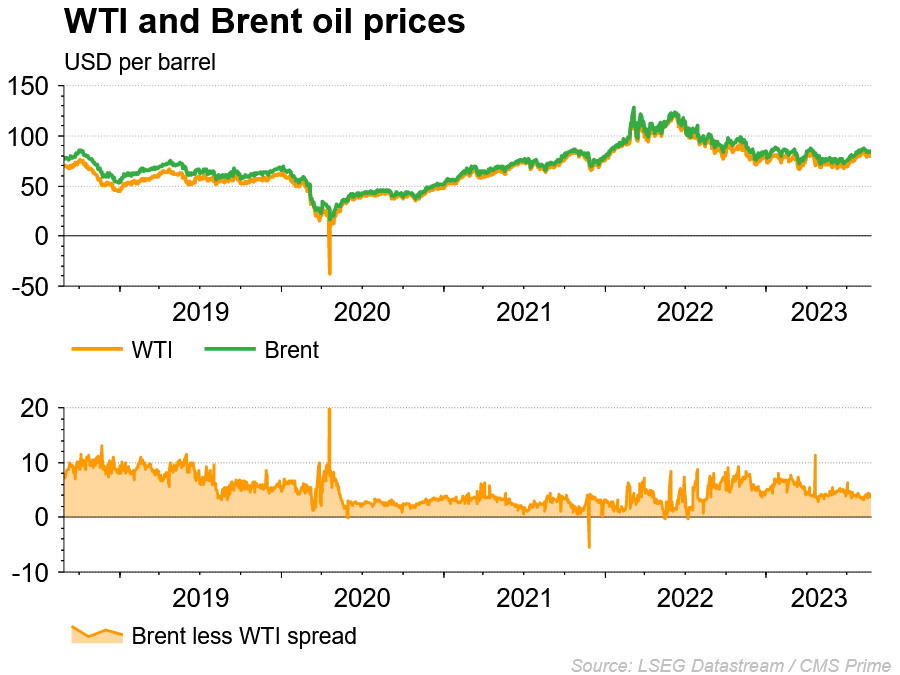

- Uncertain oil market fundamentals: The momentary bump in crude oil prices following the April 2023 announcement of production cuts was fully offset by macroeconomic concerns within two weeks. The key market features in the first half of 2023 were a lack of inventory draws (signaling weak market fundamentals) and macroeconomic concerns weighing on commodity markets in general.

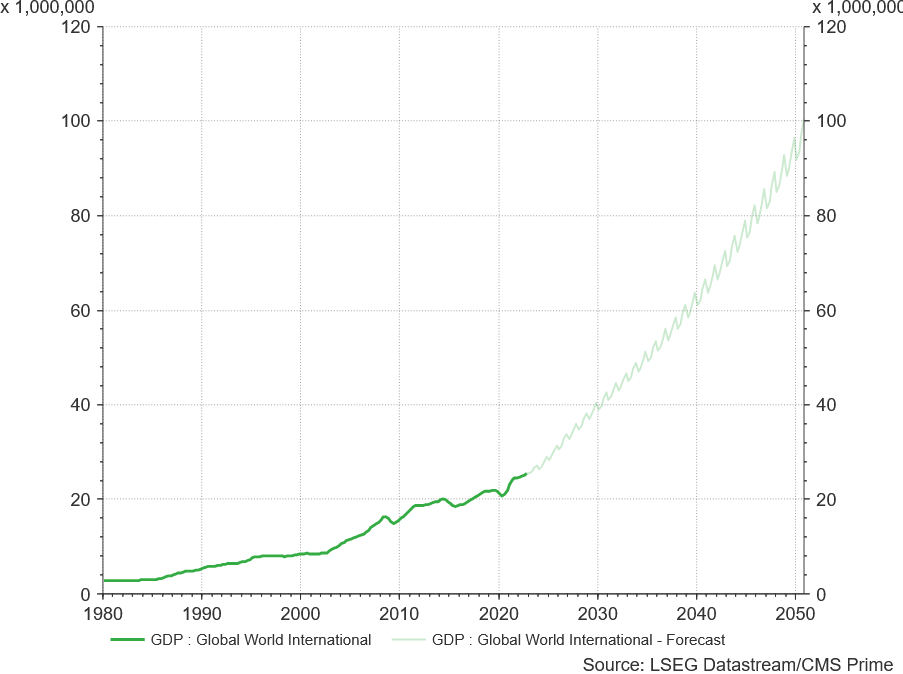

- World GDP growth: The outlook for the oil market in 2023 is influenced by the world GDP growth forecast at 3.2%. This assumes that the ramifications of the pandemic, geopolitical developments in Eastern Europe, and global financial tightening amid rising inflation do not negatively impact the 2023 growth dynamic to a major degree.

- Rising global oil production: Global liquid fuels production is forecasted to increase by 1.4 million barrels per day (b/d) in 2023. Non-OPEC production increases by 2.1 million b/d in 2023, which is partly offset by a drop in OPEC liquid fuels production. In 2024, global production increases by 1.7 million b/d, with 1.2 million b/d coming from non-OPEC countries.

The oil market’s fluctuations significantly impact currency and financial arenas. High oil demand can strengthen oil-exporting nations’ currencies, while unstable fundamentals and volatile prices trigger financial market instability. Geopolitical tensions and GDP growth projections add further uncertainty. These variables can sway investor sentiment, influencing exchange rates and prompting adjustments in central bank policies, shaping the interconnected landscape of currencies and finance.

Rising global oil production:

Rising global oil production is forecasted to increase by 1.4 million barrels per day (b/d) in 2023, with non-OPEC production increasing by 2.1 million b/d in 2023 and 1.2 million b/d in 2024. This growth in non-OPEC production is expected to offset the drop in OPEC liquid fuels production.

The United States, Canada, Brazil, Norway, and Russia are among the non-OPEC countries contributing to the increase in oil production. The US is expected to be the leading source of supply growth, with Canada, Brazil, and Guyana also hitting annual production records for a second consecutive year. In Brazil, the growth in production is attributed to increased output from floating production, storage, and offloading vessels.

Higher oil prices, spurred by Saudi Arabia’s extended voluntary production cuts, are creating incentives for non-OPEC producers to ramp up their output, allowing for growth in global oil production to continue in 2023 and 2024. The EIA projects global oil production to increase by 1.4 million b/d in 2023 and by 1.7 million b/d in 2024.

Despite the extension of OPEC+ production cuts, global liquid fuels production is forecasted to increase primarily due to growth from non-OPEC producers. The ongoing growth in non-OPEC production is expected to help meet the rising global oil demand, which is set to reach a record 101.7 million barrels per day in 2023. In conclusion, rising global oil production is driven by increases in non-OPEC countries, including the United States, Canada, Brazil, Norway, and Russia. These countries are expected to contribute significantly to the growth in global oil production in 2023 and 2024, offsetting the drop in OPEC liquid fuels production.